Summary: Understanding income tax and National Insurance is essential as UK tax thresholds remain frozen until 2031. This guide explains current income tax rates UK, UK income tax bands, and National Insurance limits in clear, simple language. It covers how tax thresholds work, why frozen bands increase tax bills over time, and how income tax and National Insurance UK deductions affect everyday earners.

If you have ever looked at your payslip and wondered why your take-home salary feels lower than expected, you are not alone. Many working professionals, business owners, and even first-time earners often find themselves confused by income tax and National Insurance deductions. With recent Budget announcements and frozen tax thresholds, understanding how these deductions work has become more important than ever.

In simple terms, income tax and National Insurance are two major deductions that fund public services in the UK. Together, they play a big role in shaping how much money actually lands in your bank account each month. With tax thresholds now frozen until 2031, more people are slowly being pulled into higher tax brackets, even without large pay rises.

This article breaks down income tax rates UK, National Insurance limits, and how both affect your earnings. Everything is explained in plain language so even someone with no financial background can follow along comfortably.

What Is Income Tax and Why Does It Matter?

Income tax is a tax charged on the money you earn. This includes salary from a job, profits from self-employment, rental income, pensions, and some returns from savings and investments. However, not all income is taxed from the first pound you earn.

In the UK, everyone is entitled to a tax-free Personal Allowance, which means a certain portion of your income is not taxed at all. Anything you earn above this allowance is taxed at different rates depending on how much you earn in total.

Understanding UK income tax bands is essential because the tax rate increases as your income moves into higher brackets. This system is known as a progressive tax structure.

What Are Tax Thresholds and Why Are They Frozen?

Tax thresholds are income limits that decide how much tax you pay and at what rate. Normally, these thresholds rise with inflation so that people are not pushed into higher tax brackets just because prices and wages increase.

However, the government has frozen income tax and National Insurance thresholds until 2031. This means the limits will stay the same even as salaries increase over time.

As a result, any pay rise, even a modest one, could mean:

- You start paying income tax when you previously did not

- A larger portion of your income is taxed

- You move into a higher tax bracket without feeling richer

According to official estimates, this freeze will result in hundreds of thousands of new taxpayers and higher-rate taxpayers over the coming years.

Current Income Tax Rates UK Explained Simply

Let us look at the current income tax rates UK that apply in England, Wales, and Northern Ireland.

Income Tax Bands and Rates UK

| Band | Earnings | Tax Rate |

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 to £50,270 | 20% |

| Higher Rate | £50,271 to £125,140 | 40% |

| Additional Rate | Over £125,140 | 45% |

This structure means you do not pay the same tax rate on your entire income. Instead, different portions of your income are taxed at different rates.

How Income Tax Bands Work in Real Life

Suppose you earn £45,000 a year.

- The first £12,570 is tax-free

- Income between £12,571 and £45,000 is taxed at 20%

- You do not pay higher-rate tax because your income does not cross £50,270

Now imagine your salary increases to £55,000.

- You still get the tax-free allowance

- Part of your income is taxed at 20%

- Income above £50,270 is taxed at 40%

This example highlights why understanding income tax bands and rates UK is crucial for financial planning.

What Happens When You Earn More Than £100,000?

Once your income crosses £100,000, the rules change significantly.

For every £2 earned above £100,000, you lose £1 of your Personal Allowance. By the time your income reaches £125,140, your entire tax-free allowance is gone.

This creates an unusually high effective tax rate, which often catches people by surprise. Many professionals, especially those receiving bonuses or variable pay, find themselves paying more tax than expected.

How National Insurance Works Alongside Income Tax

While income tax often gets most of the attention, National Insurance rates UK play an equally important role in determining take-home pay.

National Insurance contributions help fund state benefits such as:

- State Pension

- Maternity and paternity benefits

- Jobseeker’s Allowance

- Certain sickness and disability benefits

Employees, employers, and the self-employed all pay National Insurance, but the rates and thresholds differ.

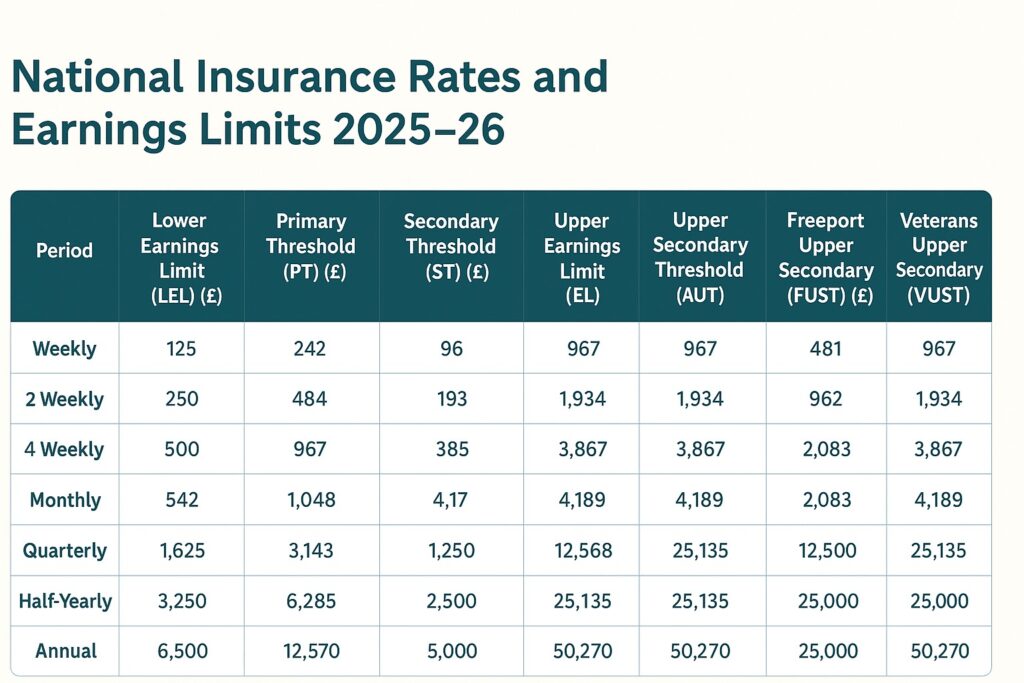

National Insurance Thresholds Explained Clearly

National Insurance is calculated based on earnings thresholds, similar to income tax. These thresholds decide when you start paying NI and how much you pay.

Workers usually start paying National Insurance when they:

- Turn 16

- Earn more than £242 per week as an employee

- Earn more than £12,570 per year as a self-employed individual

The amount is usually deducted automatically from salaries.

Recent Changes to National Insurance Rates UK

In 2024, National Insurance rates were reduced in two stages for employees. The main employee contribution rate fell from 12% to 10%, and then to 8%.

For many workers, this meant noticeable savings. For example:

- A salaried employee earning £35,000 saved close to £900 per year

- A self-employed individual earning £28,200 saved around £350 annually

Despite these reductions, frozen National Insurance limits mean more income will gradually fall into taxable bands over time.

A Simple Example to Understand Tax Bands Better

To see how income tax and National Insurance UK work together, consider an everyday UK scenario.

Imagine someone working in healthcare, education, retail, or an office-based role earning £30,000 a year. At this level, they pay basic-rate income tax and National Insurance on part of their salary. Now suppose they receive a small annual pay rise of £1,500 to help manage higher living costs.

Although the pay rise sounds positive, frozen tax thresholds mean more of that increase is taxed. Over time, repeated small rises lead to higher deductions, even if the person does not feel significantly better off.

Now take someone earning close to £50,270. A small bonus, overtime payment, or promotion could push part of their income into the higher-rate tax band. That additional income is then taxed at 40%, plus National Insurance, reducing the actual benefit of the extra earnings.

This is why understanding UK income tax bands matters not just for high earners, but also for everyday workers.

How Employers and the Self-Employed Are Affected?

Employers also pay National Insurance on employee earnings above the Secondary Threshold. This adds to the overall cost of employment and can influence hiring decisions.

Self-employed individuals pay National Insurance through their Self Assessment tax return. While the rates are generally lower, the system still relies on the same income thresholds, making planning essential.

Why Understanding UK Tax Rates Matters More Than Ever?

With tax thresholds frozen until 2031, more people will slowly pay higher levels of tax, even without major changes to their income. This makes awareness of UK tax rates explained crucial for budgeting and financial planning.

Knowing how income tax and National Insurance work together allows you to:

- Understand payslip deductions

- Plan for bonuses or overtime

- Avoid surprises at the end of the tax year

The Bottomline

Tax does not have to feel overwhelming. Once you understand how income tax rates UK and National Insurance limits work, the system becomes much clearer. Frozen thresholds mean that even small changes in income can affect how much tax you pay, making awareness more important than ever.

Whether you are an employee, self-employed, or planning your next career move, understanding income tax and National Insurance UK helps you make informed decisions. A little knowledge goes a long way in avoiding surprises and taking control of your financial future.

Disclaimer: The information provided in this blog is for general guidance and educational purposes only and does not constitute financial, tax, accounting or legal advice. iFiler, registered in England under Company Registration Number 15996173, has prepared this content to offer general insights into financial and taxation matters. Although every effort is made to ensure the accuracy and relevance of the information at the time of publication, no guarantee is given regarding completeness, accuracy or suitability for your specific circumstances.

Readers should not act, or refrain from acting, based solely on the information contained in this content. Professional advice tailored to your personal or business situation should always be obtained before taking any financial or tax related decision. iFiler accepts no liability for any loss or damage arising from reliance on the information presented in this blog.